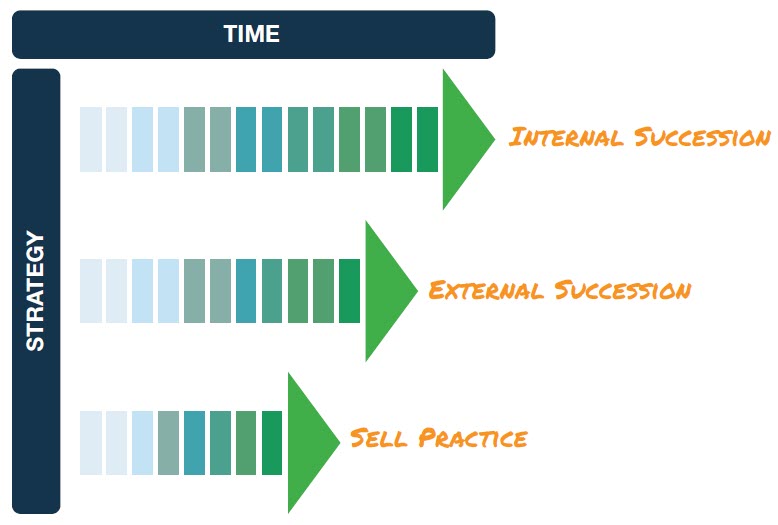

Selling your practice, for practical reasons, could be quite possibly the quickest way to transition a business. The downside is that you are passing your legacy on to someone out right – relinquishing control of your ops, staff, and clients with little to no transition. From a timeline perspective, this strategy is often driven by money, or lack of options/time for a successor.